To understand the conventional narrative often told about how to address the affordable housing crisis, check out THE NARRATIVE.

Challenges of Reducing the Cost of Providing Housing

Methods of reducing housing costs through construction efficiency, streamlined approvals and permitting processes, and land use reform may sound like promising strategies for addressing the crisis in housing affordability. After all, it would seem that unleashing developers on latent development opportunities in exclusionary communities through land use reform would increase the supply and diversity of housing products available on the market.

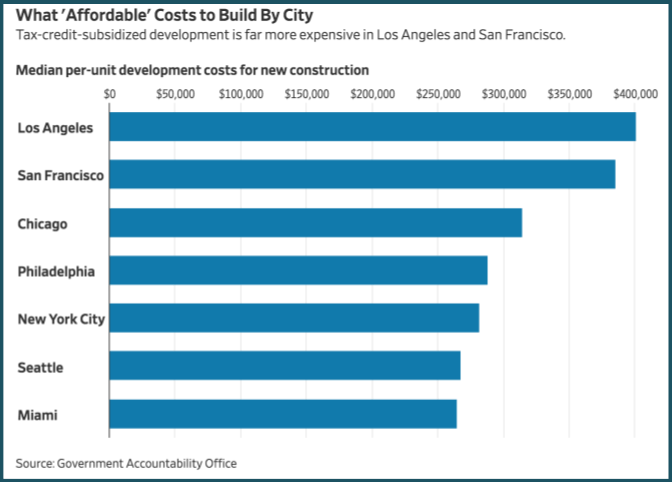

There remains, however, a significant gap between what low-income households can afford to pay for housing and the cost to buy and own a home or rent from a landlord. Moreover, the very presence of real estate professionals inevitably results in products and services unaffordable to low-income families. While pre-fabricating housing in a factory offers a significant cost savings on labor as compared to on-site construction, would skilled trades need to exchange relatively well-paid on-site construction work for lower paid factory jobs in order to reduce housing costs for consumers? Lastly, housing production is like a complex machine controlled by a series of levers that don’t operate independently from one another. Lowering one lever, such as construction costs, may result in other levers, such as land values, rising in response.

The housing market alone cannot solve the affordable housing crisis.

Challenges of Raising Household Income

Household incomes are raised primarily in three ways: public assistance programs, minimum wage laws, and workforce development. Increased household income means that more money can be dedicated to covering housing costs.

Public Assistance Programs

In part, lack of political consensus to increase funding for public assistance for low-income households prevents programs like Section 8, WIC, and LIHEAP from being made universal and permanent. But there is another issue with attempting to increase the amount of money households can dedicate towards housing.

Speculative Rental Property Investing

Since the Great Recession, institutional investors – acting through real estate professionals – have financed the widespread acquisition of residential properties formerly owned by owner-occupants and local landlords.

Expanding rental assistance programs, for instance, may also increase the rental value of residential properties, particularly in low-income and minority neighborhoods. Thereby encouraging further speculative acquisition of real estate by investors. This could result in making affordable homeownership and rental opportunities less available for those without assistance.

Minimum Wage

Raising the minimum wage is politically divisive. Not enough is understood about the economic impact of raising the minimum wage: to align with the living wage (the hourly wage required to cover average living expenses); on areas of the economy outside of employment; or relative to the business cycle.

Garnering enough political support to align the federal minimum wage with living wages will be difficult to accomplish in the near-term in the United States.

Workforce Development

Automation, jobs outsourcing, and other unpredictable changes to the future of employment opportunities in the United States may limit the effectiveness of workforce development to close the gap between household income and housing costs. Student loan debt incurred by young adults admitted into institutions of higher learning represents a major long-term expense for working age people. The over-saturation of people with advanced degrees looking for work in academia, social sciences, and other fields that lack demand for these credentials may lead to long-term wage stagnation or decline for college graduates. Student loan debt may acerbate this issue.

If housing costs cannot be reduced to meet household incomes and household incomes cannot be raised to meet housing costs, then perhaps the only way to meet the demand for housing for all households is through increased funding for affordable housing.

Challenges of Increasing Funding for Affordable Housing

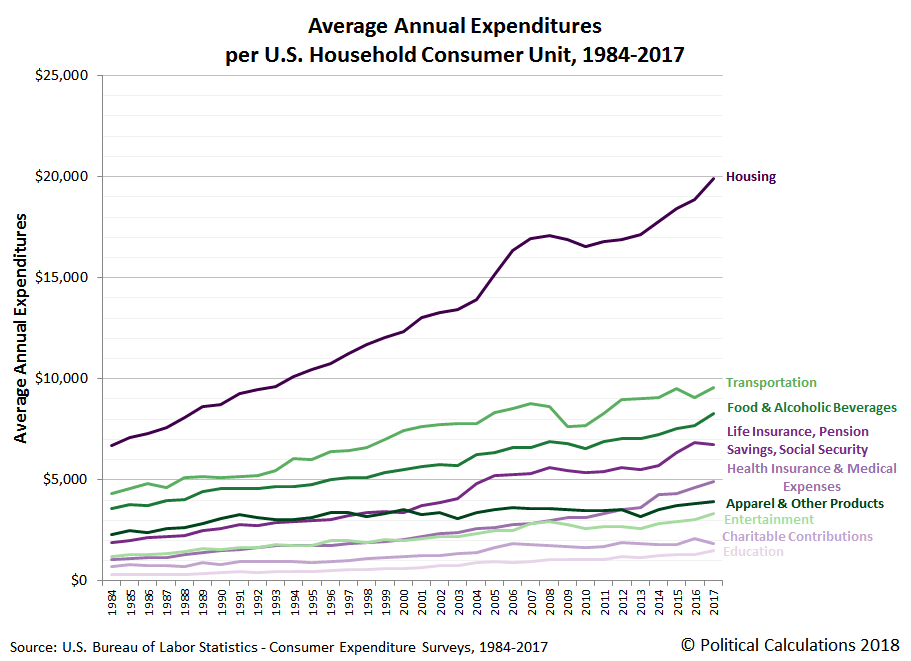

Today the incomes of low-wage workers cannot cover the costs of developing, managing, operating, and maintaining minimum standard housing, including traditional Public Housing.

Moreover, the trend in recent decades has not been to build new Public Housing, but to convert existing properties into lower-density, mixed-income communities.

As a result, 400,000 Public Housing units have been lost across the United States from a peak of 1.4 million units in 1994. This trend is unlikely to reverse in the near future.

Even if the production of Public Housing units were to vastly increase, there are legitimate reasons for replacing Public Housing units with privately-managed, lower density, and mixed-income communities. Some reasons for moving away from traditional public housing models include the history of segregation by race and income, concentration of poverty, and isolation from social, educational, and economic opportunity. Another concern is that public housing communities for families send a significant number of school-age children to public schools that are funded by local property taxes to which public housing does not contribute because of its tax exempt status.

Bureaucratic systems struggle to accurately predict, provide for, and accommodate changing household demands over the period of time that residents live in subsidized housing. According to HUD, “holders of housing vouchers have received assistance for an average of 9.1 years, while the average Public Housing resident has lived in such a unit for 10 years.” When, for instance, program participants want to house an aging relative, an adult child, or unmarried partner, or start a home business, or sublease space in their home, publicly-assisted housing programs often lack the nimbleness to accommodate them.

The Costs of Meeting All Housing Demands

Some estimates project a cost of $20 billion per year over five years to build enough housing nationwide in the US to meet the demand for the millions of households who currently cannot afford market rate housing. The Urban Institute predicts a cost of $100 billion to house the 8.2 million American households who currently cannot afford their monthly rent through Housing Choice Vouchers.

From where will the revenue come to fund the housing subsidies necessary to cover the gap between what low-income households can afford to pay and the cost of providing housing?

Real Estate as a Domestic Tax Shelter

Passive income and capital gains can be sheltered from taxation by donating to non-profit organizations, purchasing Low Income Housing Tax Credits, and owning and investing in real estate. If those individuals and corporations capable of navigating the US Tax Code will avoid paying taxes, who will end up paying for increased affordable housing funding? The incomes of wage earners and salaried workers would need to be taxed in order to generate enough revenue to pay for the subsidies required to make housing both profitable for real estate professionals and affordable to low-income families.

Recent tax policies, like the Tax Cuts and Jobs Act, have limited the Home Equity Interest Deduction and Property Tax Deduction, and capped the size of mortgages with Interest Deductions. At the same time, municipal budgets and local taxation has also increased. With many homeowners impacted by these changes, is it politically desirable, or even feasible, to raise additional income tax revenue from living wage workers in order to subsidize valuable real estate assets?

Is there political will to reform the tax policies that allow capital gains and passive income to be sheltered from taxation through real estate? If the tax advantages of investing in real estate are removed, what is the likelier outcome: investing in real estate will remain constant and capital gains and income tax revenue with increase, or investing in real estate will decrease and tax revenue with remain neutral? If it would lead to divestment from real estate, would this contribute to further housing shortages?

Should we continue an approach to housing affordability that relies on taxing workers’ wages and salaries in order to subsidize developers’ tax-exempt real estate investment income?

Public and Private Authoritarian Development

Will issues arise when people are provided with something, like housing, without having acquired the knowledge of how to provide, maintain, and improve that thing for themselves? Far from liberation, isn’t there a risk of ensuring that the recipients of subsidized housing become dependent upon professionals to finance, maintain, and repair their housing on their behalf for generations to come?

Clearly, there are many challenges associated with conventional approaches to addressing the affordable housing crisis.

To learn about some of the implications of those challenges, continue to THE TRUTH.