To understand the central problem at the heart of the affordable housing crisis, check out THE QUESTION.

Over the last four decades, the most popular approaches to closing the gap between household incomes and the prices of market rate housing have been to:

I. Reduce the cost of providing housing for the marketplace;

II. Raise household income; and

III. Increase funding for affordable housing.

I. Reducing the Cost of Providing Housing for the Marketplace

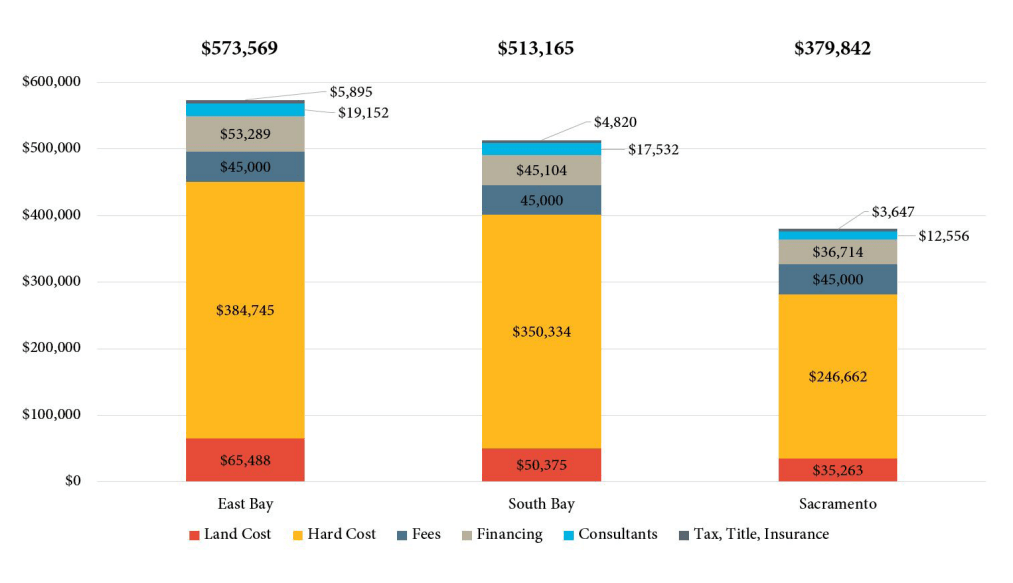

The price for which housing is sold or rented is derived, in large part, from fixed costs associated with providing housing. Fixed costs include hiring architects, engineers, attorneys, contractors, realtors, and property managers, and paying property taxes, debt service, and investor returns. By reducing some or all of these costs, it may be possible to provide housing at a lower price without impacting the profit margin of sellers or landlords.

Construction Cost Savings

One popular approach to reducing overall costs of housing is through construction efficiencies. Strategies for reducing construction costs include prefabrication, modular construction, design-build coordination, and other time-saving and labor-reducing methods.

Traditional construction requires buildings to be built entirely on-site by licensed contractors earning competitive wages. Prefabrication and modular construction, however, allows building components to be manufactured off-site by laborers and then rapidly assembled on-site by contractors. Design-build coordination attempts to reduce costs through better planning and design in the early stages of a project so that unexpected and expensive issues do not emerge later in the development process.

Streamlining Approvals and Permitting

Another cost appears during the regulatory approval and permitting phase of a project. Often, developers must hire land use attorneys, code consultants, and design professionals, and pay service fees to ensure that projects comply with land use ordinances, building codes, and other regulatory requirements. These costs can be reduced by creating a predictable and easily navigable process that streamlines approvals and permitting for housing developments.

Exclusionary Zoning Reform

In a climate of decreasing government funding for affordable housing, one popular approach to making housing more attainable for moderate-income households is to increase housing production and supply in order to promote the creation of naturally-occurring affordable housing through filtering. Housing filtering is often seen as a market-based approach to creating housing that is affordable to more people.

One way people try to increase the supply and diversity of housing products is by liberalizing zoning regulations.

Vast areas of the developed world have been zoned as open space or large lot, detached, single-family, and single-use development in order to preserve property values and support long-term debt financing. As a result, even when there is demand for small lot, attached, multifamily, and mixed-use development, and there are developers willing to provide for that demand, land use regulations and zoning commissions often prevent that type of development from occurring.

Creating model zoning codes along with incentives or requirements to adopt those codes is one strategy for reforming land use regulations. Re-zoning and up-zoning may enable developers to supply the market with more housing products that moderate-income households can afford to purchase or rent. Increasing the production and diversity of new housing of various kinds may also decrease the demand for existing older housing stock and lower prices sufficiently for working class households to afford without subsidies. Some of the work of allowing smaller lots and greater residential density may become necessary in response to, not only affordability, but market preferences as well.

II. Raising Household Income

Income Assistance Programs

Another approach to making housing more affordable, which can be used in conjunction with cost reductions, is to increase household purchasing power. This can be accomplished through income assistance, higher wages, and workforce development.

Income assistance can include rental, down payment, and other forms of payments for living expenses like health insurance, home heating, and groceries. These public assistance programs can help to increase the amount of household income that recipients may dedicate towards housing expenditures. Expanding existing public rental assistance programs, as some have advocated, may improve access to affordable housing for low-income families.

Increasing Household Income

Nowhere in the United States can a minimum wage earner working 40 hours a week afford to pay Fair Market Rent for a two bedroom dwelling unit.

Throughout the country, the minimum wage is too low for a worker to pay for housing on their own without being underhoused, rent burdened, or overworked.

One approach to addressing this issue is to raise minimum wages to align with cost of living indexes and a 40 hour work week. Another is through workforce development that aims to improve workers’ earning abilities with skills training and education.

Minimum Wage

Conservative economists theorize that raising the minimum wage decreases overall employment, while some empirical evidence supports the claim that modest increases to the minimum wage can raise workers’ earnings with minimal impact on employment growth.

Workforce Development

Increasing household income through training and educational opportunities to improve workers’ desirability and hireability in the job market may help some families to house themselves without subsidies. The U.S. Department of Housing and Urban Development (HUD) promotes integrating jobs programs and housing services with the aim of closing the gap between the experience required for jobs that pay a living wage and current skill levels of working age people. Graduates of higher education programs tend to earn more than less-credentialed job-seekers.

III. Increasing Funding for Affordable Housing

During World War I and under the New Deal, the Federal government of the United States built Public Housing for working families. By removing the profit margin of rental housing and the expense of local property taxes, the government was able to provide high quality apartments in well-managed complexes at rents that workers could afford.

Today non-profit affordable housing developers largely depend on publicly-funded programs like housing tax credits, rental assistance, development grants, and property tax breaks.

Closing the gap between housing costs and household incomes may depend on the ability of governments to raise additional revenue through taxes. At the same time, institutional investors, high net worth individuals, sovereign wealth funds, and pension funds seek out opportunities for investing capital and sheltering income from taxation. But since charitable contributions, like donations to non-profit organizations, can be deducted from taxable income, private philanthropy may offer another funding source for affordable housing.

Summary

Lowering the costs of providing housing for the marketplace, raising household incomes, and increasing funding for affordable housing are typically seen as a comprehensive solution to the affordable housing crisis.

To learn about some of the challenges associated with lowering housing costs, raising household income, and increasing funding for affordable housing, continue to THE CHALLENGE.