This is the first part of a two part series looking at the Desegregate CT platform. To read Part 2, click here.

plat·form

noun

• a raised level surface on which people or things can stand.

In June 2020, Desegregate Connecticut publicly launched an initiative to address residential segregation with statewide zoning reform. Through an ongoing series of news media articles and well-attended virtual meetings, the role of restrictive land use regulations, like exclusionary zoning, are being discussed. Curious residents, academics, and design and planning professionals from around the State are seeing presentations about increasing housing costs, barriers to development, and the segregation of people by race and income.

Desegregate CT, in collaboration with many local, regional, and statewide organizations, is advocating for changes to local zoning ordinances that would allow for greater production and availability of a variety of housing products in Connecticut’s urban, suburban, and rural communities. By increasing the supply of housing, this collaborative advocacy group hopes to play a significant role in making cities and towns more affordable places in which to remain or relocate. Ultimately, Desegregate CT would like residential neighborhoods across the state to be racially and economically integrated.

The rapid mobilization of individuals, legislators, and dozens of professional organizations over the summer of 2020 to support a movement to desegregate Connecticut has been impressive. In this work, there is much to commend. DEMOCRATIZE DEVELOPMENT would similarly like to see the reduction or elimination of residential segregation resulting from unlawful or unethical discrimination. To list all of Desegregate CT’s accomplishments and instances of commonality with DEMOCRATIZE DEVELOPMENT would be repetitive. For that reason, the following commentary will focus only on constructive criticism and areas of divergence.

The intent of the first part of this two part series is to take a critical look at the platform upon which Desegregate CT has built its policy recommendations. DEMOCRATIZE DEVELOPMENT believes that movements ought to be informed by the most accurate information possible so that decisionmakers can make the best decisions available. Just as housing should be built on a solid foundation, statewide legislation should be based on accurate information. The following commentary is intended to bolster the foundation upon which Desegregate CT assembles its movement. Doing so many broaden the movement’s audience, include greater diversity of thought, and build consensus across political lines. Thus far, the movement has been dominated – to its detriment – by narrow Progressive, neo-liberal, and politically left-leaning interests.

History of Residential Segregation in Connecticut

According to the Desegregate Connecticut website,

Connecticut’s racial and economic segregation results from decades of backwards government programs and policies.

Connecticut’s communities have been segregated in a variety of ways since their inception. In the 17th century, local night watchmen kept lookout for outsiders trying to come into town. Early on, farmers occupied the rural hinterlands, merchants settled close to harbors, laborers squatted around the periphery of town centers, and native tribes lived on reservations. By the late-19th century, distinct ethnic enclaves emerged within cities and their surrounding suburbs. Yankees, Blacks and waves of Irish, German, Italian, Polish, and Russian immigrants lived where land was available to improve and cultivate, improved property was attainable, landlords would rent them rooms they could afford, preferred religious institutions were located, specialty grocery stores were present, and familiar languages could be heard.

In response to rapid industrialization and development, local governments in Connecticut’s cities began to play an important regulatory role in housing through fire safety codes and tenement laws. For instance, the City of New Haven, at the urging of Progressive social reformers concerned about the living conditions of laborers, passed an ordinance prohibiting the construction of backyard tenements in 1898. Seven years later, the State of Connecticut adapted existing local city ordinances to establish a set of statewide standards for tenement housing.

It was not until the private market struggled to adequately address the national housing shortage during the First World War that the Federal government got involved in development. Multifamily residential communities, like Seaside Village in Bridgeport, were built and temporarily managed by the government in cities with major wartime manufacturing operations and limited supplies of housing to serve workers. More than a decade later, the Great Depression spurred the Federal government’s involvement in housing finance through New Deal legislation.

Residential segregation by socioeconomic status in America predates government involvement in housing policy.

Regulations and Housing Costs

The Desegregate CT website goes on to say that:

Our laws prevent us from having an adequate housing supply and a diversity of housing for people of all incomes and backgrounds.

Significant reductions to public health standards, zoning regulations, housing ordinances, municipal waste policies, and building codes would be required in order to significantly lower the cost of developing housing for the private marketplace. For instance, should developers be allowed to construct housing without toilets, baths, sinks, and other sanitary facilities? Should all single-family homeowners be allowed to open a boarding house by right? Should residential living space be permitted in all cellars? Should urban property owners be able to opt out of paying for and using municipal waste collection services? Should sleeping be allowed in windowless rooms?

Merely allowing higher density dwellings will not substantially lower the cost of producing housing for a consumer market.

Ignoring or failing to recognize why laws were first adopted may risk recreating the undesirable conditions that inspired their initial creation. In the mid-20th century, as household incomes steadily rose in the United States, a growing consensus emerged around the importance of preventing and remediating environmental pollution. Improving air and water quality, cleaning up contaminated soil, limiting noxious industrial uses, protecting wetlands, and preserving open space became major concerns of State and Federal legislation in the 1960s and 70s.

For example, many suburban communities in the postwar era saw demand on municipal infrastructure and services, developed land area, and the population of lower-middle class residents and schoolchildren rapidly increase. Towns in New Haven County had to drastically raise their property taxes to cover the costs of providing services and educating children. In 1963, Branford taxed property at a rate of 50 mills, while North Haven’s mill rate climbed to that same level by 1970. Communities were often unprepared and ill-equipped to quickly transition from rural towns into built-up suburbs.

In accordance with environmental and budgetary concerns, Connecticut municipalities sought to limit residential development in environmentally sensitive areas and concentrate on attracting tax-positive commercial businesses and industry to their towns through their decennial Plans of Conservation and Development, zoning regulations, and economic development policy. In 1968, the Fair Housing Act sought to open up formerly exclusionary suburban communities to a wider segment of the metropolitan population by prohibiting racial discrimination in housing.

Having learned from experience or observation, concern about a second wave of tax-negative residential development is a major reason why suburban towns have restricted growth over the last 50 years.

Condominiums, which privately maintain and provide their own infrastructure and services, became a preferred method for developing housing in some communities in the latter third of the 20th century.

Government Involvement in Housing and Urban Development

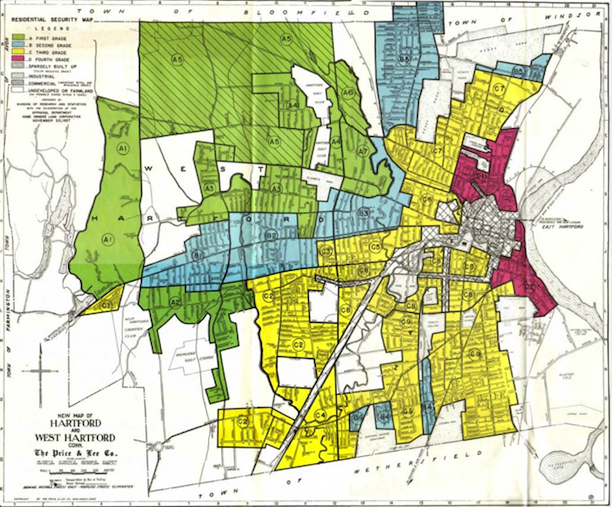

[The United States Housing Authority] authorized the construction of racially segregated public housing, and the [Federal Housing Administration and Home Owners’ Loan Corporation] spearheaded the obstruction of government-sponsored homeownership and private investment in areas with “inharmonious racial groups.” These areas, deemed unfit for investment, were “redlined,” or colored red on appraisal maps of cities across the country.

In the early-20th century, Progressive social reformers like Emma Rogers in Connecticut advocated for government-regulated minimum standards for housing through statewide tenement laws, local public health codes, and other land use and development regulations. The intent was to improve public health and safety for residents in so-called “slum” neighborhoods. One of the unintended results was to increase housing construction, repair, and maintenance costs, raise rents, create new utility fees, and make many pre-existing buildings becoming non-compliant with the new regulations. During the Great Depression, these higher costs became burdensome and many tenants fell behind on their rent and bills while owners defaulted on mortgages, property taxes, and utility payments.

To prevent a nationwide collapse in residential mortgaging, Congress passed New Deal Legislation in 1933 and National Housing Acts in 1934 and 1937, which authorized the creation of the Home Owners’ Loan Corporation (HOLC), Federal Housing Administration (FHA) and United States Housing Authority (USHA), including local Public Housing Authorities (PHAs).

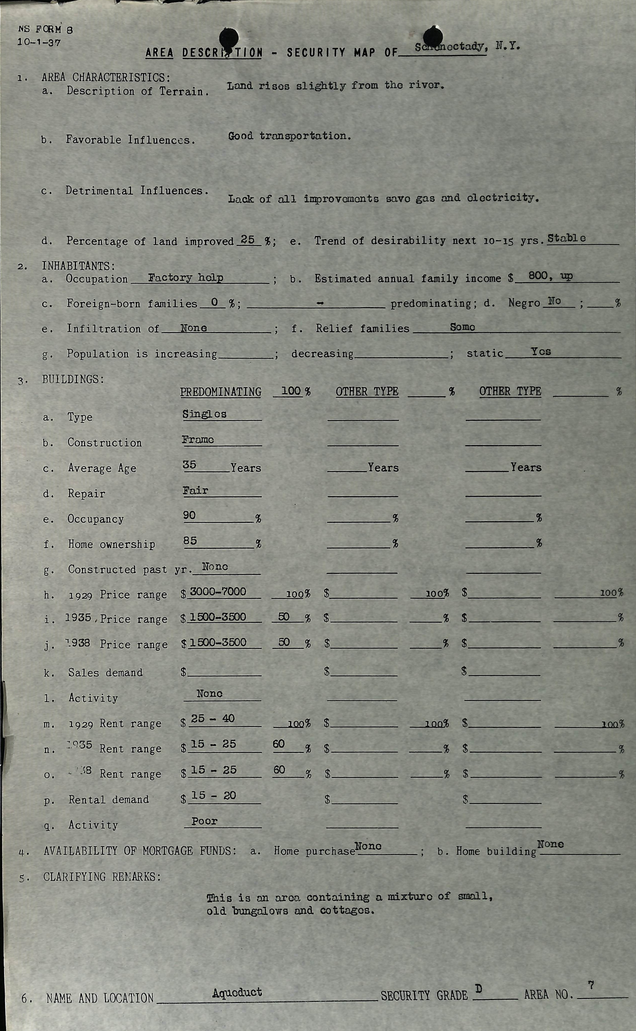

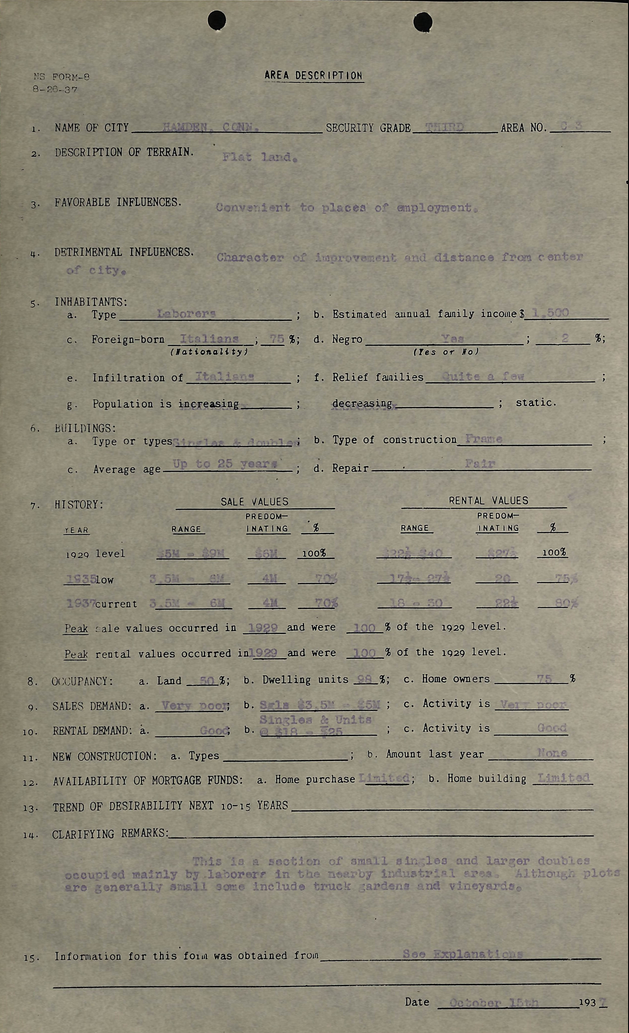

HOLC was given two tasks: refinance Building & Loan Association home mortgages at risk of default; and assess the riskiness of residential lending within segments of local housing markets. For the second task, HOLC surveyed metropolitan areas throughout the country in the mid-to-late 1930s. Federal and local surveyors considered several factors when evaluating the lending security of neighborhoods, including demographics, income of residents, employment status, sales data, rental prices, private lending activity, age and condition of housing, access to utilities, and quality of improvements on the land, as well as the opinions of local realtors.

Neighborhoods with unemployed, lower-income, and ethnic minority families and few recent home sales, low rents, little private lending activity, older non-compliant housing stock in poor condition, and lack of sewers tended to rank low. The lowest ranked neighborhoods were labeled “Grade D” and colored red on maps published by HOLC. Academics often assert that neighborhoods were “redlined” due to the presence of Black residents and mixed-use and multifamily rental housing stock. So people are often surprised to learn of examples of White, suburban, and residential communities being given “D” grades. In fact, 92% of the population of redlined areas was White. At the same time, there are also instances of neighborhoods home to Black residents not being “redlined”.

The term “redlining” is frequently associated with a racially-discriminatory lack of lending activity. In their reports, however, HOLC surveyors explicitly stated that they did not intent to imply that good mortgages did not exist or could not be made in D-grade neighborhoods. In actuality, most HOLC refinancing of short-term, high-interest rate mortgages with longer-term, lower-interest rate mortgages in the early-to-mid 1930s was done in neighborhoods subsequently labeled “C” and “D” Grade.

Some lenders found that skilled laborers in modest homes were more reliable mortgagors than upper management professionals in upscale housing.

Likewise the FHA was very active in cities like Bridgeport, New Haven, and Hartford immediately before and during the Second World War. The FHA helped make small, low-interest loans available to property owners for repairs and improvements to existing housing stock. While FHA residential mortgage insurance is often associated with new postwar Whites-only suburbs, much of its activity throughout the late 1930s and early 1940s was concentrated on lending for improvements to aging houses and existing structures many of which were in “redlined” neighborhoods. There are also instances of the FHA insuring mortgages for new residential subdivisions for Black families.

When it came to long-term residential mortgage lending in the mid-20th century, lenders and insurers appear to have been primarily concerned about the stability and predictability of neighborhoods. This was at a time of dynamic and rapid urban change. Neighborhoods prone to economic instability or highly unpredictable change were avoided by lenders and insurers of long-term home mortgages. Neighborhoods, whether inhabited primarily by Black or White families, with economic stability and the appearance of predictability, through deed restrictions and zoning regulations, were attractive to long-term lenders and insurers.

Essentially, in residential areas deemed desirable for long-term home mortgages, according to underwriting criteria, FHA offered mortgage-backed loan insurance and, in less desirable areas, FHA offered access to short-term home improvement loans. In the ladder half of the 20th century, nonwhites were living in both of these kinds of areas. Additional programs also became available to address surplus and substandard housing. In mixed-use and distressed residential areas deemed undesirable for traditional loans, FHA insured rehabilitation loans. Residential properties beyond the point of rehabilitation were often redeveloped under Federal Public Housing and Urban Renewal programs.

The properties that were non-compliant with public health, land use, and building regulations often required investments above the FHA loan cap. Moreover, many of these properties housed residents who could not afford a rent increase commensurate with a substantial rehabilitation project. As a result, some residential properties and property owners in cities could not qualify for loans.

Lending to people with low incomes or unreliable sources of income, poor credit history, small savings, or little collateral can be risky. Same with severely deteriorated buildings that violate housing codes and lack sufficient market demand to repay the loan. When risky mortgages are made, they often come with less favorable terms, including shorter repayment periods, higher interest rates, and higher down payments. Repaying a loan for something as expensive as code compliant housing requires a long-term commitment, stable income, and interest payments on top of the principal loan amount. If recipients default on these loans, the lenders may be labeled predatory. Avoiding lending in these situations, on the other hand, may be perceived as unethically discriminatory.

Perhaps a bigger issue than either predatory lending or redlining is the insistence by Progressives that housing be provided through means that require expensive debt financing.

Under the Housing Act of 1937, Federal funding was made available to condemn, acquire, and demolish “slum” communities in cities across Connecticut. In their place, new rental dwellings that met minimum health and safety standards and were affordable to working families were built. Until the early 1960s, Public Housing complexes were allowed to be racially segregated. In the 1940s and 50s, federal housing projects built in neighborhoods where a single race predominated were sometimes reserved for that race, while developments in mixed-race neighborhoods might be segregated by building.

In the mid-20th century, Public Housing vastly improved the quality of affordable rental accommodations for working families in cities. The program also helped alleviate a housing crisis during World War II. In recent critical accounts, these achievements have been overshadowed by the initial authoritarian “slum clearance” delivery process, later economic development rationale, and subsequent concentration of impoverished residents, physical deterioration of buildings, and incompetence and corruption present within some PHAs.

The HOLC surveyors adopted existing private lending practices as one consideration for determining the financial riskiness of hyperlocal housing markets. In some ways, the Federal government spearheaded efforts to make public investments in “risky” neighborhoods and encourage private investors to do the same.

The Federal government made enormous investments in “redlined” neighborhoods through HOLC mortgage refinancing, FHA home improvement loans and insurance, and the Public Housing and Urban Renewal Programs.

According to Desegregate CT,

[T]he urban renewal movement caused the dislocation of many communities of color. In 1949, the Federal Housing Act allocated public funds for “slum clearance” with the goal of improving the quality of life for people in neighborhoods considered “blighted.” The effect was quite the opposite, with neighborhoods torn apart and new housing quickly falling into disrepair.

New Haven, for example, received more federal urban renewal money per capita than any other city. It used this funding for projects such as the Oak Street Connector, a highway system that displaced 886 families and uprooted an entire neighborhood. Today, New Haven is working on projects to remedy the harmful outcomes of these developments.

As a result of Urban Redevelopment and Renewal projects in New Haven in the 1950s and 60s, an estimated 30,000 people in 10,000 households had to relocate. The majority (56%) of those people were identified as being White. Residents identified as Black may have been disproportionately impacted, but urban renewal dislocated more White communities than “communities of color”.

In the mid-20th century, the Oak Street neighborhood was a dense, mixed-use, working class, and Jewish neighborhood increasingly becoming home to Black migrants from the Southern United States. The neighborhood was built atop a former creek bed that had been used by tanners until it was filled in the 1880s. Prior to the completion of Interstate 95 in the 1960s, car traffic between New York and Boston traveled along Route 1, which existed as a two lane street in New Haven. The Oak Street neighborhood was physically deteriorating, losing population, snarled with traffic, sitting on contaminated soil, and lacking the market demand necessary to cover clean up, infrastructure construction, and building improvement costs.

The New Haven Redevelopment Agency used Federal funding to condemn, acquire, and clear the land, build infrastructure including sewers, roads, and public parking facilities, and consolidate small lots into larger parcels in order to attract private developers to build apartment towers, office buildings, and medical laboratories. Since 2012, the City has created new zoning districts, offered tax breaks, and applied for Federal and State transportation grants to build bridges, layout new streets, and widen existing roads in order to accommodate the private development of medical offices, research laboratories, and parking structures.

The Oak Street Connector may have been replaced by Downtown Crossing in nomenclature, but the methods and goals of past Urban Renewal programs and current economic development policies are nearly indistinguishable.

In recent decades, Community Development Block Grants, Low Income Housing Tax Credits, Hope VI, Empowerment Zones, Enterprise Zones, New Market Tax Credits, Choice Neighborhoods Initiative, Opportunity Zones, and other State and Federal housing programs have invested in formerly “redlined” neighborhoods.

The Location of Subsidized Housing

Restrictive zoning, costly review processes, and arbitrary impediments thwart affordable and multi-family housing development. Perhaps as a result, Connecticut’s affordable housing efforts have overwhelmingly located in areas of concentrated poverty. Between 2011 and 2013, Connecticut allocated 48.6% of its affordable housing tax credits to neighborhoods where the poverty rate was greater than 30%.

Each living unit in a housing project typically costs hundreds of thousands of dollars to develop. Those costs can be repaid in one of two ways. First, tenants can pay the full costs through their own rental payments. Second, the public, through local, state, and federal subsidies, can cover the gap between the revenue needed to develop and operate the housing and the rent that low-income households can afford to pay.

Developers tend to pursue affordable housing projects in communities where they are confident the local legislature will provide tax breaks and help secure other state and federal subsidies. Communities with sewers, highways, job centers, and transit service also attract multifamily developers. Budget-conscious councils in towns without supportive infrastructure often do not attract subsidy-seeking developers.

Conclusion

Readers of the Desegregate CT website will likely get the impression that unethical racial and economic discrimination under official government policy is the primary cause of today’s residential segregation. Hopefully, this post helps to paint a more complex and accurate history of housing in Connecticut. This history is troubling enough without the need to make exaggerated, misrepresented, or inaccurate statements.

One of the toughest challenges facing the State today is how to meet the housing demands of low-income families. In the mid-20th century an FHA program insured home mortgages, which allowed developers to build large Whites-only planned residential communities of detached single-family houses at prices that modest wages could afford. In fact, monthly mortgage payments for a new house in Levittown on Long Island in the 1950s were less than Public Housing rents in New York City.

In some cases, houses today regularly sell for hundreds of thousands of dollars in Levittown. What were affordable starter homes several decades ago have become prohibitively expensive for many working families to buy. High property values are partly the result of restrictive zoning, which limits new supply and raises prices on existing houses. For the most part, however, the steep ascension of real estate values in postwar suburbs resulted from owner-initiated home improvement projects such as dormers for new attic bedrooms, rear and side additions, finished basements, and porches and decks. In other cases, formerly Whites-only suburbs have become inclusive and diverse over time.

DEMOCRATIZE DEVELOPMENT is in favor of extending the opportunities and responsibilities of homeownership to everyone that desires it. One of the issues that must be reckoned with is that many of the affordable Cape-style starter home developments built in the postwar era do not meet current housing and building code requirements for bedrooms per occupant, fire safety, energy efficiency, and accessibility. Additionally, forests have regrown on former farm land and other open spaces in recent decades – increasing clearance and site preparation costs. Addressing residential segregation, like housing affordability, is a major challenge that eludes simple answers.

The long-term success of any structure depends on the strength of the foundation, or platform, upon which it is built.

To continue on to Part 2 of the series about Desegregate CT, click here.

{kind=link}

{kind=link}